How Card Payments Work: Transaction Processing and Costs For Your Business

We review the participants of the card payment process, fees associated with different parts of the process, and what to consider when choosing a payment processing provider.

While cash may still be king in a few diminishing use cases, according to the Federal Reserve, consumers make over 60% of their payments with cards (credit cards—32% and debit cards—30%).

We’re so used to POS (Point Of Sale) and POP (Point Of Purchase) terminals and paying with cards from our devices that it doesn’t feel like this process involves numerous parties working in perfect harmony together to take money from a cardholder’s account and deposit it into the merchant’s, whether at a restaurant, online business, or anywhere else where payments are made.

In this article, we’ll go over the participants of the card payment process, the fees associated with different parts of the process, and the factors to consider when choosing a payment processing provider that’s right for you.

What exactly happens when you make a card payment?

Once the cardholder authorizes the transaction, the payment starts being processed. This comes down to several steps:

- Cardholder (most commonly) initiates the transaction by submitting their payment details to the merchant digitally or in person.

- The merchant requests the payment, which means that the payment processing solution asks the cardholder’s bank to authorize the transaction.

- The request goes through the appropriate card association (Visa, Mastercard, Discover, American Express, etc.), which forwards it to the issuing bank.

- The issuing bank (cardholder’s bank) checks the funds’ sufficiency, runs any necessary checks, and, if approved, settles the transaction through the payment provider and the card association.

- Money is deposited into the merchant’s account at the acquiring bank.

- Once the payment cycle is completed, changes are reflected in the cardholder and merchant accounts.

Who takes part in card payment processing?

As you can see, many pieces of the payment infrastructure move every time a card is swiped, inserted, or tapped. Here’s who we’re dealing with:

- In most cases, the cardholder is the one making the transactions, but in certain situations, the merchant can initiate recurring payments or other pre-authorized transactions (like that one subscription service you needed a reminder to cancel).

- Card associations like Visa, Mastercard, Discover, American Express, UnionPay (China), or JCB (Japan) are responsible for creating the cards. Each company builds a vast network of businesses and countries that accept cards issued by them.

- Issuing bank – cardholder’s bank.

- Acquiring bank – merchant’s bank.

- Payment processor—To accept card payments, you need a payment processing provider to plug into this financial infrastructure. The payment processing provider a business uses affects personal and corporate data security, processing cost, payment speed, regulatory compliance, and user experience.

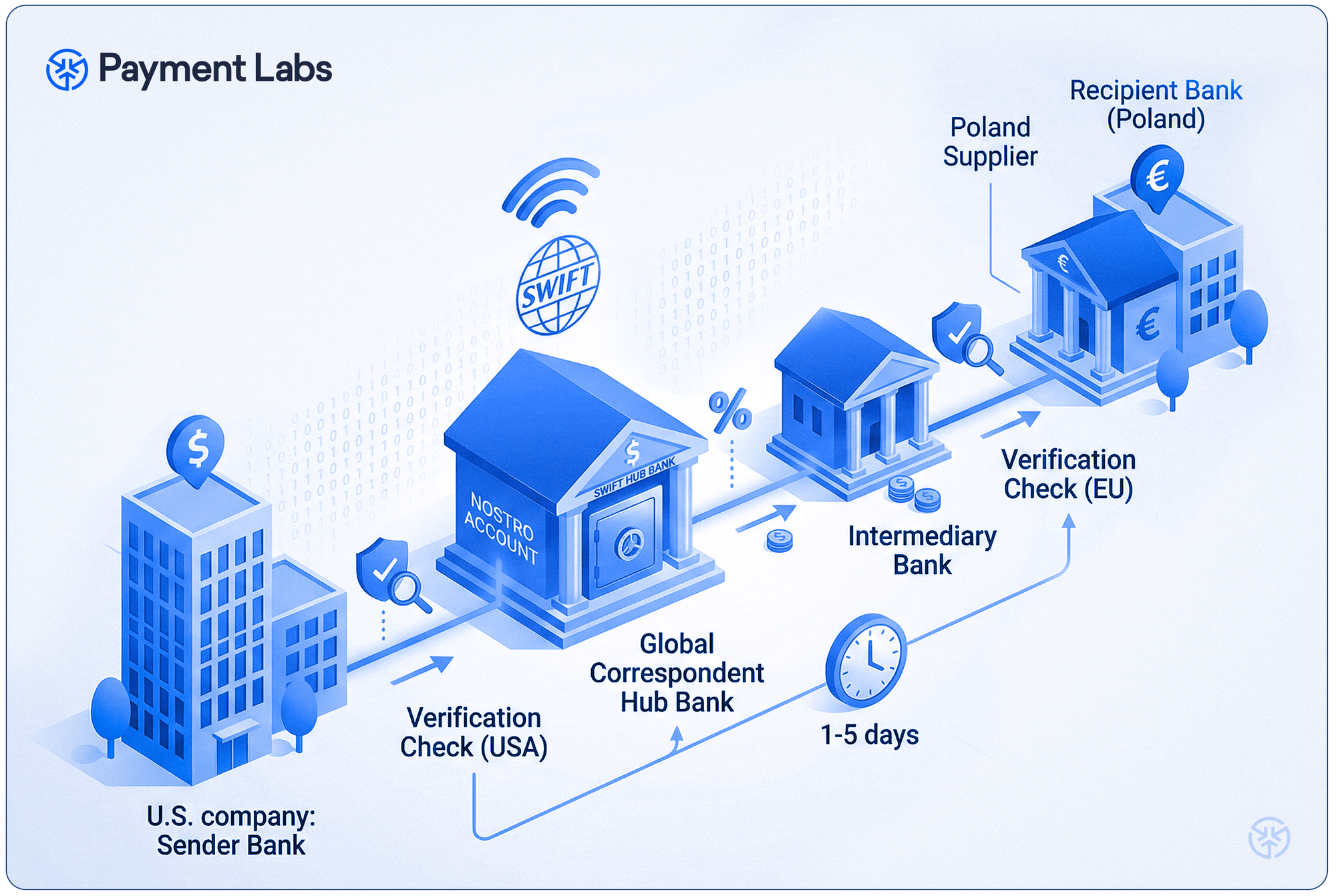

What is the processing difference between domestic and international card payments?

We all want international payments to be as easy, cheap, and fast as local ones. However, as financial crime threats become more sophisticated, international regulations and security measures are strengthening.

While our current technology is amazing and automates everything, cross-border payments still have to go through much more than they do within one country’s payment infrastructure.

More complex fraud prevention and compliance, more participants, higher risk, and unstable exchange rates all factor into the cost of international payments.

Who charges what fees when you make a card payment?

With so many parties involved in processing every transaction, one can only wonder who is paying them and how much.

Well, every participant in the payment process applies their own fees. Here is what you’re paying for and what to clarify with your bank, card association, and payment provider.

- Interchange fees – The merchant’s bank pays the cardholder’s bank to handle the transaction.

- Scheme fees – Card associations get the card assessment fee from the issuing and acquiring banks.

- Processor fees – The payment processing provider charges a fee to manage the communication and data between all these participants. This fee can be per transaction, a percentage of the amount, or a regular subscription cost.

- Fixed fees – Your bank, payment processor, or other service providers may charge custom fees depending on the payment type and other factors.

- Payin – When money is deposited into a wallet or a card, the service provider often charges a payin fee.

- Chargeback fee: When the cardholder successfully disputes a transaction, the merchant’s bank is charged a fee to encourage clear customer communication and reduce fraud.

- Cross-border fees: The cardholder is usually charged if they send money to another country. The merchant, too, may pay a fee if their bank or payment provider charges them.

How do you pick an optimal payment processing provider for your business?

Since 60%+ of all customers mainly use cards for payments, you must be very careful about the payment processing technology you rely on.

Payment Labs provides an all-in-one (payin and payout) payment processing for esports, sports, creator, and NIL payments. The platform allows businesses to manage entry fees, brand deals, and any other payments they need to accept.

Most businesses we talk to mention the same payment processing challenges they faced with past technology providers or want to avoid in the future, such as:

- Hidden transaction fees can significantly hurt the cash flow when a business and payment volume start to scale.

- Technology lock-in – Business owners try to avoid becoming too dependent and tied to a software provider.

- Regulatory and industry standards compliance – A payment processing system is only as good as its transactions are compliant with PCI DSS, global AML and KYC rules, GDPR, and any other relevant regulations in the countries and industries where you plan to work.

- The growth constraints of a payment processing system can halt the momentum of your business growth.

- Chargebacks management needs to be intuitive for the cardholder and predictable for the merchant. Make sure your payment processor offers a flexible dispute resolution process and transparent chargeback fee logic.

- Lack of support when you need a human to solve your payment processing issues and help with getting the most out of your solution.

- Subpar fraud prevention leads to constant worry and suspicion as you can’t check every transaction manually. Consider the provider’s transaction monitoring procedures, fraud prevention settings, and transaction data handling standards when considering a payment processor.

- Cross-border payment cost and reach: Determine whether you can process international transactions with the countries you need without additional fees and at a good exchange rate.

Here’s how Payment Labs fits into your card payment processing life:

At Payment Labs, we enable businesses to accept and make cross-border payments in 140+ currencies across 180 countries. We stand out in cost with our low flat-rate fees and wide-ranging currency support. When it comes to software, we get the most praise for the solution’s usability and transaction efficiency.

We’re proud to offer an all-in-one payment platform where businesses seamlessly process global card payments as well as other payins and payouts. Schedule an intro call today so we can handle all your payment processing needs!