Fedwire and CHIPS – All You Need to Know about Large Transactions in the US

Fedwire and CHIPS (Clearing House Interbank Payments System) are both cornerstone parts of the local payment rail system of the USA.

Imagine you’re a bank in the United States, and you are looking at two large transfers.

- One is a multimillion payment your client initiated where speed is of the essence.

- The other is one large transaction that settles all your daily payments with a wide range of financial institutions.

You’d wire the first one through Fedwire and the second one through CHIPS. In this article, we’ll cover everything you need to know to make informed decisions on the fly when dealing with large wire transfers inside the USA.

Fedwire and CHIPS (Clearing House Interbank Payments System) are both cornerstone parts of the local payment rail system of the USA.

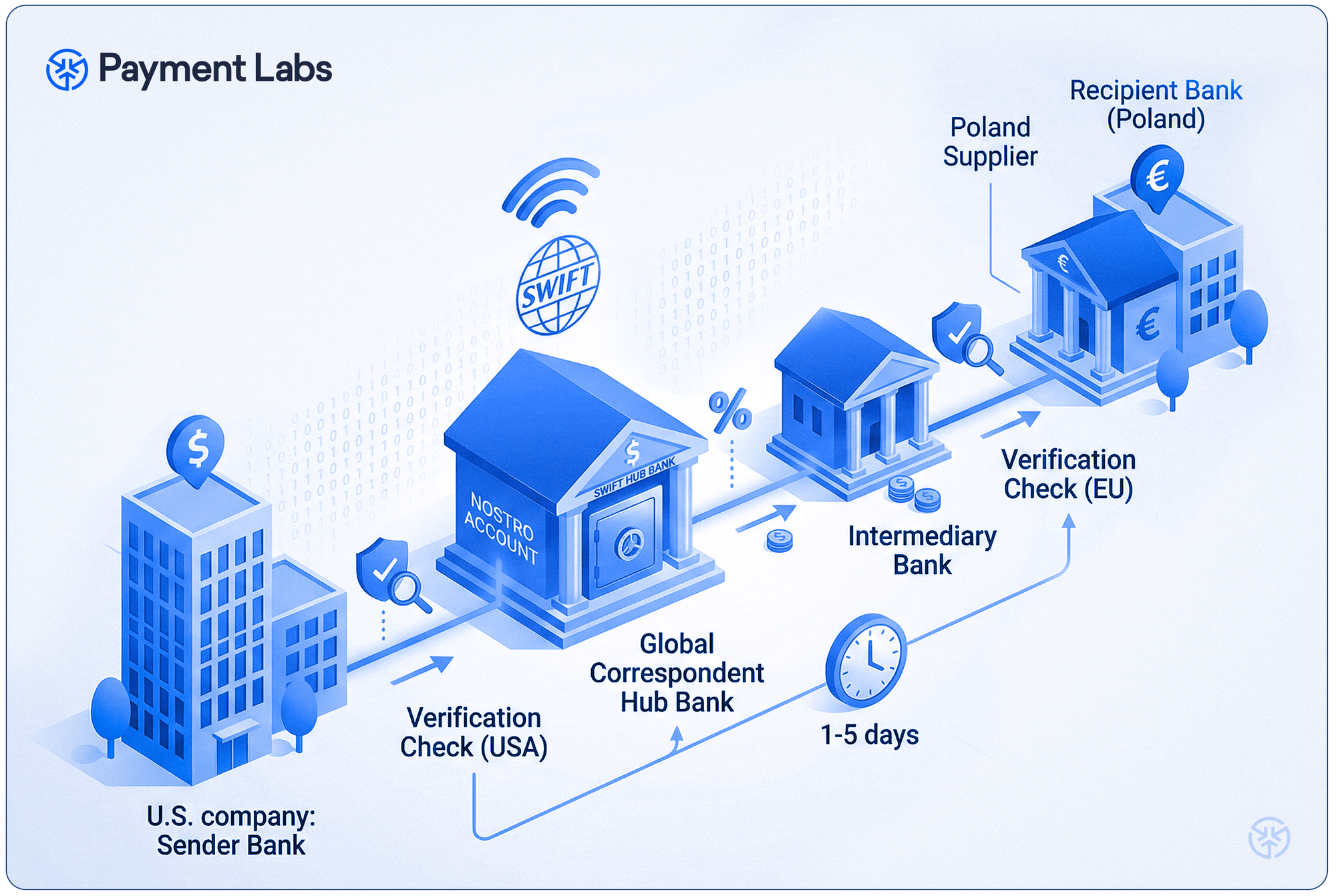

Fedwire is the electronic funds transfer system created by the Federal Reserve to settle large digital transactions within the country. CHIPS is an exclusive tool used by a select group of major financial institutions to net interbank settlements to cut the cost of transfers made on Fedwire.

While most small- to mid-size consumer and business transactions are handled through ACH transfers or newer systems like FedNow, CHIPS and Fedwire efficiently handle high-value transfers.

These Clearing and Settlement Systems are created specifically to move large sums of money between U.S. banks and for international transactions settled in USD.

What is Fedwire?

Fedwire is the main way of handling real-time gross settlement of high-value transactions in the US.

Just as railroads and highways were needed to enable economic growth, the financial sector needed an efficient way of handling an ever-growing number of transactions. Enter Fedwire, the dedicated system for high-value transfers managed by The Federal Reserve Banks.

Electronic payments have existed since the early 1900s, and in 1918, the US Federal Reserve launched Fedwire (Fedwire Funds Service)—revolutionary tech that replaced physically moving money, doing paper-based deals, or using the telegraph for interbank communications.

The Federal Reserve Wire System in 1953 (source)

Many decades since, Fedwire now connects well over 9,000 financial institutions in the US and continues to introduce innovations like ISO 20022 migration and the planned expansion to Sunday operations in 2028.

What is CHIPS?

In 1970, a consortium of banks in the US created CHIPS (Clearing House Interbank Payments System). The volume of CHIPS transactions averages roughly two-thirds of the volume of all Fedwire transactions. According to The Clearing House, CHIPS handles $1.8 trillion daily transactions between the consortium’s 50 direct participants.

CHIPS allows member banks to figure out amongst themselves who owes whom and how much. And then, at the end of the day they settle the tab with the Federal Reserve, paying way less than if they made millions of instant transactions through Fedwire during that time.

CHIPS was created to provide select US banks and branches of foreign banks with a cost-saving tool for using Fedwire. A privately-held alternative that allows its members to move trillions between their accounts without sending the money back and forth unnecessarily. This makes for much more efficient liquidity management and best of all – it costs less.

From the start, the focus of CHIPS was to allow for cheaper clearing and settlement of transactions through netting. This means calculating the final balance and sending payments once a day instead of forwarding each one instantly.

How the CHIPS net settlements work

CHIPS uses a proprietary netting process to enable lower transaction costs. Throughout the day, CHIPS keeps score of who owes whom across all members. At 6 p.m. ET, CHIPS runs the math and settles the remaining balances through Fedwire.

Participant banks significantly reduce Fedwire fees since CHIPS transactions between the participants offset the final obligations. CHIPS transfers netted settlement instructions to Fedwire, as a result, the participants pay fees on $1 for every $29 in settled value.

The role of CHIPS in international/cross-border payments

95% of CHIPS payments are the U.S. dollar leg of a funds transfer that begins or ends in another country. CHIPS handles the dollar settlement side of international payments with SWIFT acting as the network that carries the transaction messages.

This works through correspondent banking. Foreign banks use an intermediary to route payments to one of the 50 CHIPS members. Since CHIPS is supervised by the federal government, barring access to it is one of the key elements in the U.S. sanction policy.

How to choose between CHIPS and Fedwire for high-value transfers

- Settlement process/speed - With CHIPS, netted transfers happen once a day, whereas Fedwire transfers are real-time.

- Cost - When dealing with CHIPS, your fees are lower, which comes with longer settlement time.

- Transaction size - The average transaction size for CHIPS is $3 million. Fedwire is commonly used for high-value transactions of all sizes.

- Membership - To use either system, you need to be a member of CHIPS or Fedwire, but it is much simpler to opt in for Fedwire.

- International suitability - CHIPS in tandem with SWIFT is an important part of international payments in USD. Fedwire is used primarily for domestic U.S. settlements.

Fedwire vs CHIPS – roles in the financial ecosystem

Fedwire is the foundation of high-value payments in the U.S., and the primary way of final, guaranteed settlement with the Federal Reserve.

CHIPS sits one level above. It connects 50 major financial institutions in one deal-making space, running the day’s calculations before anything goes out to Fedwire. This way members only pay Fedwire fees on the balances remaining at day’s end, not all transactions.

While Fedwire is primarily domestic, CHIPS is the backbone of global USD settlement, with 95% of transactions having a cross-border leg.

Both CHIPS and Fedwire have recently embraced the ISO 20022 messaging standard which enables richer, more structured data to be included in each transfer, reducing compliance holds.

Operating hours and transaction limits of CHIPS and Fedwire

- Fedwire operates Monday through Friday with an operating window from 9 p.m to 7 p.m. ET the next day. The transfers must be initiated by 6 p.m. ET. And the transfer ceiling is set at $10 billion. In 2028, the service plans to cover Sunday too.

- CHIPS operates 9 a.m. to 6 p.m. ET on weekdays without a per-transaction cap. If a transfer is made when CHIPS is closed, payments are resolved through Fedwire directly.

Fedwire and CHIPS vs FedNow

FedNow is an instant payment infrastructure available 24/7 developed by the Federal Reserve for smaller retail and business payments up to $10M. FedNow is not as widespread as Fedwire (1500+ vs 9000+ members) and many participants are receive-only, but it is useful for weekend, holiday, and urgent payments.

When to use which - Fedwire, CHIPS practical use cases

When processing high-value transactions, the choice between CHIPS and Fedwire comes down to the speed, fees, and access to CHIPS.

Use Fedwire when:

- Speed is critical and you can’t wait until end of day

- Your bank doesn’t have a CHIPS member correspondent relationship

- It’s a domestic U.S. transfer

Use CHIPS when:

- You’re moving large volumes of high-value payments

- The transfer is part of cross-border USD settlement

- The payment doesn’t need to settle instantly.

How to use Fedwire and CHIPS

You need to be a member of Fedwire or CHIPS to make a transfer on either system. Both Fedwire and CHIPS are open for new members, and it’s relatively easy for a financial institution to opt into Fedwire on the Federal Reserve’s website. Transactions through both systems are irrevocable so the correctness of payment instructions is crucial.

CHIPS is an exclusive community whose requirements include the organization's net worth, maintaining adequate liquidity, and adhering to strict operational and risk management standards. However, as a financial institution, you can easily establish correspondent bank relations with one of the 50 members.

Final thoughts

The U.S. high-value payment system is layered, but once you understand how Fedwire, CHIPS, and FedNow fit together, the right choice for any transfer becomes straightforward. If you’re looking to build a payment infrastructure on top of these systems, that’s where we come in. If you have any questions or need assistance automating your payments, don’t hesitate to contact us.

At Payment Labs, we specialize in creating dedicated cross-border payment systems that fit your needs. We have unique expertise in esports prize payments, sports payments, NIL payouts, and agency solutions that simplify fast and compliant global payments with low, flat-rate fees. Our solution automates payments so you can focus your time on growing your business instead of managing payments.