The Guide to Online Payment Security Methods

When managing payments, it’s essential to recognize the sensitivity of having access to a customer’s personal and banking information and how to secure the process.

Part 1: Security Foundations in Payment Data

Understanding the landscape

When managing payments, it’s essential to recognize the sensitivity of having access to a customer’s personal and banking information and know how to secure the payment process. For example, in the United States, possessing someone’s account and routing number allows unauthorized access to withdraw funds—an action similar to intruding into someone’s home, taking something, and leaving with it. Therefore, it is essential to treat all payment-related data with utmost confidentiality. This principle extends to credit cards and identifiers for platforms like Zelle and Venmo. Safeguarding sensitive information in today’s digital-first world is the top priority in any financial transaction, and a proactive approach to data protection is paramount.

Key challenges organizations face

The key challenges organizations face with security and payment data with online payments will almost always be the human element. The most challenging part invariably lies in the weakest link of your security system, which is often associated with the human aspect—the element crucial for the functioning of a company. It’s impossible to restrict access to a single individual and designate them as the sole executors of tasks related to sensitive payment data. Implementing rigid measures, where everyone else must navigate through a gatekeeper, would be counterproductive. As a result, the primary challenge will almost always be the human element, especially in today’s global remote-first digital world. Thus, businesses must ensure that every individual, whether new to the company or a seasoned veteran, understands the importance of data protection.

Fundamental elements that form the foundations of security in payment data

Security foundations of payment data and the importance of online payment security methods have changed over time. In today’s landscape, online banking and digital payment methods are predominant. With this shift, cyber-attacks have become more pervasive, exploiting the increased vulnerability of data stored in the cloud compared to traditional methods like faxing or in-person transactions. The acceleration towards online platforms and digital payments has also intensified in the post-pandemic era. As a result, online payment security needs to be at the forefront of any company that deals with any part of the payment process.

The fundamental elements in securing this digital realm of payment data includes comprehensive encryption measures. Leaving data in plain text poses a substantial risk, as it becomes easily visible. Therefore, robust encryption, at a high level, is crucial. Additionally, separating systems is essential, with distinct environments like production and development serving as dedicated spaces so that production and non-production data is segregated.

Adhering to the principle of least privilege is another important aspect of securing payment data. Granting access based on necessity is essential. For example, an intern should only have access to production environments if explicitly required for their tasks. Regular password rotations and frequent changes to encryption keys also contribute to maintaining a secure infrastructure. Practicing good overall hygiene in data management reinforces the system’s resilience against cyber threats. By implementing these measures, organizations can establish a robust defense against the evolving landscape in payment data security.

How the threat landscape has evolved over the years

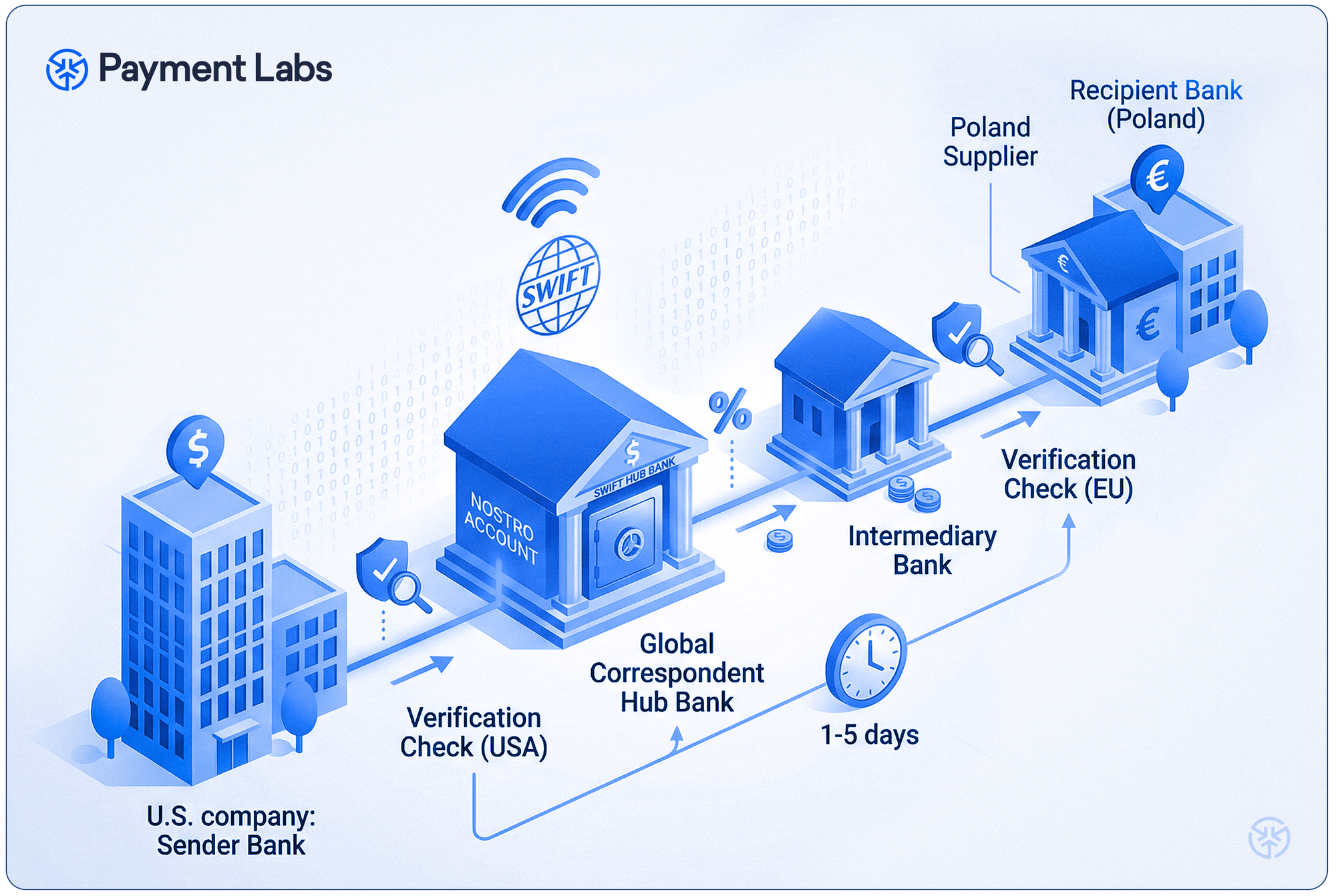

In the current landscape, the entire financial infrastructure has transitioned to an internet-based model. The emergence of neo-banks, fully operational online banks, has become a prominent aspect of this digital shift, mainly made popular in the post-pandemic era. Traditional practices of walking into a branch and physically presenting identification for wire transfers are no longer the preferred payment method. The preference is for quick, convenient, and seamless digital transactions.

With this reliance on online platforms comes its share of risks, and the threat landscape has evolved. The vulnerability of online accounts to breaches has also become more widespread. Extortion has increased in the digital realm, particularly with the rise of cryptocurrencies. Unlike the demand for unmarked bills, contemporary extortion can involve requests for cryptocurrencies such as Bitcoin. In this environment, payment organizations need to balance speed and convenience with a heightened awareness of cybersecurity risks. As the financial landscape evolves, individuals and organizations must implement robust security measures to safeguard sensitive client data against potential breaches and digital threats.

The role of encryption and authentication in security foundations for online payment data

Encryption plays a part in securing sensitive data by converting it into an encoded format and making it indecipherable without the corresponding keys for decryption. It’s also essential to distinguish between encryption and hashing, where passwords are hashed in a one-way direction. Encryption, on the other hand, operates in two directions. The data is encrypted; a single key is used for encryption and decryption, or separate keys can handle each function. This flexibility is essential, especially when dealing with sensitive information like banking details. Sending encrypted data to a bank wouldn’t work when providing instructions. Decryption is necessary for comprehension.

Authentication, which means verifying the identity of the person claiming to be who they are, is another integral component of data security. Methods such as username-password pairs and identity verification contribute to the authentication process. In the context of security frameworks, authentication, encryption, and hashing form an important triad for protecting sensitive financial data. These elements collectively strengthen the overall security architecture of an organization, ensuring the confidentiality and integrity of sensitive information.

Approaching risk assessment and management when establishing online security foundations in payments

Start by formulating well-defined security policies while recognizing that policies are always subject to evolution. Businesses focused on rapid growth might exhibit a higher risk tolerance, whereas longer-established businesses with a substantial footprint tend to have a more conservative risk posture. Conducting vendor assessments is a critical practice in this regard. Customers commonly request SOC 2 reports or employ security questionnaires. SOC 2 is a voluntary compliance standard for service organizations developed by the American Institute of CPAs (AICPA), which specifies how organizations should manage customer data. The standard is based on the following Trust Services Criteria: security, availability, processing integrity, confidentiality, and privacy. This evaluation is essential, as it provides insights into the potential risks associated with working with vendors, regardless of their size, and ensures alignment with established policies and procedures.

How organizations can use new technologies to protect online payment data

Think about the importance of prioritizing security first and adhering to the principle of least privilege. Encrypting data is crucial, and while achieving SOC 2 Type 2 certification may not be an immediate necessity, adopting a security-first mindset will enhance resilience. When a data breach occurs, the response often involves an all-hands-on-deck approach. Establishing policies, procedures, and Standard Operating Procedures (SOPs) in advance is instrumental. In the event of a crisis, following a pre-established checklist and procedures proves significantly more effective. This proactive approach ensures a measured response even in high-stress situations, allowing for a methodical resolution of the crisis.

The role of continuous monitoring in maintaining online payment data security

Continuous monitoring and vigilance are critical when safeguarding a payment system against intrusion attempts. Cybercriminals, particularly ransomware groups, typically target larger entities for higher payouts. As an organization expands, so will its attractiveness as a target, necessitating constant monitoring. Employing a web application firewall and securing employee devices are also essential measures.

Remaining updated on the latest developments is vital, especially concerning zero-day vulnerabilities—exploits in the wild that attackers can immediately exploit. Notable instances, like the Log4J incident, have showcased the global impact of such vulnerabilities. In 2017, Cloudflare experienced the Cloudbleed incident, emphasizing the potential vulnerabilities even for significant internet entities. Staying vigilant and proactive in monitoring and implementing preventive measures is paramount to keeping a payment system safe against evolving cyber threats.

Strategies organizations should employ to ensure payment data compliance

Many banks offering financial services require fintech companies to adhere to the SOC 2 Type 2 framework. As previously noted, SOC 2 serves as a comprehensive set of standards and policies that companies adapt to their specific needs, creating a standardized framework applicable across various business stages. Achieving SOC 2 certification involves undergoing an audit to ensure that stated policies are not only in place but also of high quality. It goes beyond assertions and makes sure that organizations adhere to a structured framework. Companies adhering to these frameworks tend to establish a robust security foundation and sound policy infrastructure. However, it’s essential to recognize that even with stringent frameworks in place, the possibility of attempted breaches remains. Acknowledging this possibility and continuously implementing preventative measures is of utmost importance.

Creating a security-aware company culture

As we covered in this guide, employees will always represent a potential weak link in the security chain, particularly vulnerable to social engineering tactics. Social engineering is also increasingly prevalent, with people falling victim to tactics like call and text message spoofing. Instances of compromised Twitter accounts and email breaches are also common occurrences.

Implementing and enforcing two-factor authentication (2FA) with tools like Google Authenticator is a more secure approach than relying on SMS for 2FA. SMS-based 2FA is known to be insecure, especially when considering potential vulnerabilities, such as SIM card hacking, which is particularly prevalent when traveling internationally. Hacking the SIM card or conducting a SIM clone through a call to the cell provider can even result in the complete takeover of a phone number.

With the rise of fintech companies, the risk of data breaches and attempted intrusions is also increasing. As a result, employee training is more important than ever in addressing and mitigating these evolving security challenges. Organizations can enhance their security by educating employees and keeping sensitive customer payment data safe in an evolving digital landscape.

At Payment Labs, we provide secure global payments with the ability to transact in 140+ currencies across 180 countries. Reach out to our team to learn more today!

Stay tuned for part 2 of our Guide to Online Payment Security Methods: Privacy Strategies for Secure Payments – Ensuring Compliance.