IBAN Payments – One Payment Standard to Enter 87 Countries and Territories

The financial world strives for unification and standardization to handle enormous transaction volumes faster and with fewer mistakes.

The financial world strives for unification and standardization to handle enormous transaction volumes faster and with fewer mistakes. In that light, the Swift network and the IBAN standard are the two most important global payment initiatives that stand as monuments to trade globalization over the last 50 years.

So right off the bat, here’s an instant clarification in the Swift vs IBAN debate so you can navigate between the two:

- IBAN payments can be used for any type of payment transaction. Your IBAN points to the specific bank account within one of the financial institutions from 87 countries and territories that use the IBAN standard.

- Swift codes or BIC are used for transactions between financial institutions. When your bank sends a cross-border payment to another bank via the Swift network, they create a Swift message, and the IBAN is one of the key data pieces to include as part of the Swift code, also known as the Bank Identification Code (BIC).

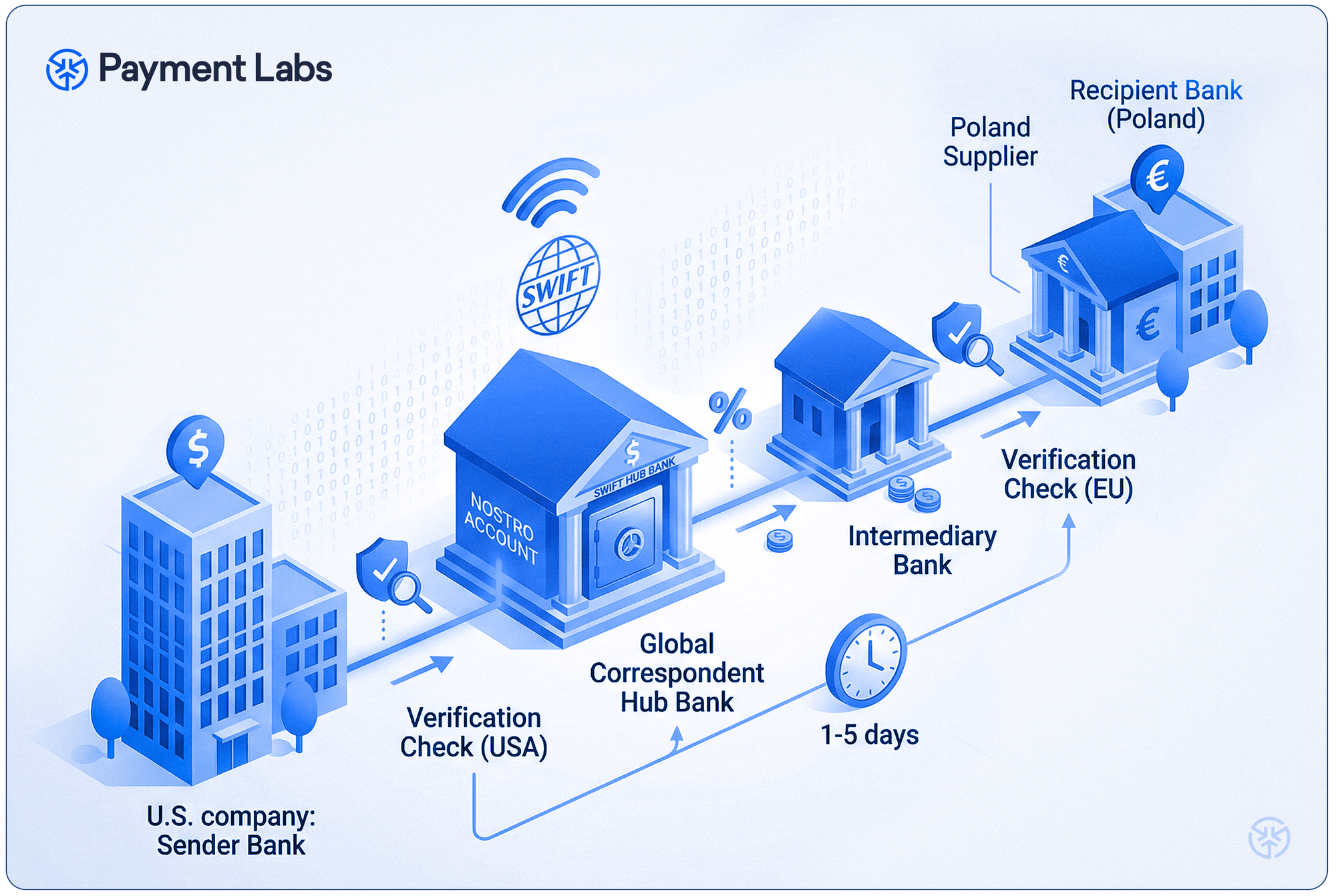

In the previous installments of this series, we reviewed the Swift network in detail and compared it to using local payment networks for cross-border payments.

And today we’ll review all you need to know about IBAN payments and how to use them to unlock the European market as well as 50+ other countries for your business.

What is an IBAN?

IBAN is the most widely accepted and recognized standard used to identify bank accounts in all 87 countries that use the International Bank Account Number standard.

Created for and primarily used in the European Union, it’s also widely accepted and/or recognized in the Middle East, the Caribbean, North Africa, and Asia. Even though major economies like the US or China don’t use IBAN, many institutions there can process these payments. This, however, rarely needs to be done since all those countries use the Swift network to communicate about their international transactions.

IBAN consists of up to 34 alphanumeric characters that contain all necessary information about a specific bank account.

How to read an IBAN – Structure of an IBAN

An IBAN consists of 2 parts.

- Header

- Country codes use standard formats like DE for Germany or GB for Great Britain.

- Check digits—This is a standard IBAN error detection system that uses a mathematical algorithm called Modulo 97 to check the validity. However, banks generally verify all the data on their end, too.

- BBAN – Basic Bank Account Number

- BBAN can be up to 30 characters. For example, Norway’s BBAN is 15 characters, and France’s is 27. Each country sets its own algorithm for the BBAN structure, but generally, it includes the bank code, branch code, currency, an account number within the bank, and sometimes additional check digits.

A short history of IBAN

IBAN was created to allow the European Union to have a single standard for payments to finally cut the amount of errors and payment processing time both domestically and between the EU member states.

In 1988, the European Committee for Banking Standards (ECBS) published the first IBAN proposal. The International Organization for Standardization (ISO) quickly adopted the new standard as ISO 13616.

After the European Union made IBAN the standard for all domestic payments, they were able to create SEPA. Single Euro Payments Area connects 26 central banks of the European Union in a single interbank network, which uses IBAN as a domestic standard for all participants to achieve full interoperability.

Until now, the standard is used most in the eurozone, but since it was introduced in the 90s it has spread far beyond the EU due to its usability and the snowballing network effect.

What is ISO 13616?

ISO 13616 is the official standard that defines the most current globally accepted IBAN format. It is managed by ISO (International Organization for Standardization), and the most recent version of the IBAN standard is ISO 13616 published in 2020.

How is the IBAN standard managed?

Unfortunately, no financial standard is perfect, so there needs to be continuous improvements to IBAN to keep up with the demands of international trade. Within ISO, the Technical Committee (TC) 68 oversees financial services, including implementing changes to the IBAN standard or ISO 13616. To change a system of this international importance, one of the national standards bodies or important industry stakeholders can submit a proposal to modify the IBAN standard to TC 68. There, member countries’ representatives analyze the submission and make final decisions with a vote.

Which countries use IBAN?

According to the 2024 IBAN registry published by Swift, there are 87 countries that comply with the ISO 13616 standard for IBAN formats. So you don’t have to download the full document, here’s the full list:

🇦🇩 Andorra

🇦🇪 United Arab Emirates

🇦🇿 Azerbaijan

🇧🇦 Bosnia and Herzegovina

🇧🇪 Belgium

🇧🇬 Bulgaria

🇧🇭 Bahrain

🇧🇮 Burundi

🇧🇷 Brazil

🇧🇾 Belarus

🇨🇭 Switzerland

🇨🇷 Costa Rica

🇨🇾 Cyprus

🇨🇿 Czech Republic

🇩🇪 Germany

🇩🇯 Djibouti

🇩🇰 Denmark

🇩🇴 Dominican Republic

🇪🇪 Estonia

🇪🇬 Egypt

🇪🇸 Spain

🇫🇮 Finland

🇫🇰 Falkland Islands

🇫🇴 Faroe Islands

🇫🇷 France

🇬🇧 United Kingdom

🇬🇪 Georgia

🇬🇮 Gibraltar

🇬🇱 Greenland

🇬🇷 Greece

🇬🇹 Guatemala

🇭🇷 Croatia

🇭🇺 Hungary

🇮🇪 Ireland

🇮🇱 Israel

🇮🇶 Iraq

🇮🇸 Iceland

🇮🇹 Italy

🇯🇴 Jordan

🇰🇼 Kuwait

🇰🇿 Kazakhstan

🇽🇰 Kosovo

🇱🇧 Lebanon

🇱🇨 Saint Lucia

🇱🇮 Liechtenstein

🇱🇹 Lithuania

🇱🇺 Luxembourg

🇱🇻 Latvia

🇱🇾 Libya

🇲🇨 Monaco

🇲🇩 Moldova

🇲🇪 Montenegro

🇲🇰 Macedonia

🇲🇳 Mongolia

🇲🇷 Mauritania

🇲🇹 Malta

🇲🇺 Mauritius

🇳🇮 Nicaragua

🇳🇱 Netherlands

🇳🇴 Norway

🇴🇲 Oman

🇵🇰 Pakistan

🇵🇱 Poland

🇵🇸 Palestine

🇵🇹 Portugal

🇶🇦 Qatar

🇷🇴 Romania

🇷🇸 Serbia

🇷🇺 Russia

🇸🇦 Saudi Arabia

🇸🇨 Seychelles

🇸🇩 Sudan

🇸🇪 Sweden

🇸🇮 Slovenia

🇸🇰 Slovakia

🇸🇲 San Marino

🇸🇴 Somalia

🇸🇹 Sao Tome and Principe

🇸🇻 El Salvador

🇹🇱 Timor-Leste

🇹🇳 Tunisia

🇹🇷 Turkey

🇺🇦 Ukraine

🇻🇦 Vatican City State

🇻🇮 Virgin Islands

IBAN alternatives

While IBAN is one of the most far-reaching and universal financial standards, there are billions of people in the countries that use their internal systems instead of it. The United States, Canada, China, India, Japan, Australia, and other major economies rely on their internal systems for domestic payments. Even though you can find banks that will work with IBAN payments in most countries, the processing time and fees will be higher.

IBANs role in cross-border payments

Like Swift, IBAN has become one of the cornerstones of the international financial infrastructure. Whether you’re making a cross-border transaction from your bank or with an app like Wise, IBAN will most likely be used to route your money at some point.

Even though the world of global payments is immensely better thanks to systems like IBAN or Swift, as a business owner, you need a payments management tool to rely on these legendary systems and leverage cutting-edge technology for faster, cheaper, and safer transfers.

At Payment Labs, we specialize in creating tailor-fit payment solutions for use cases like esports prize payments, sports payments, NIL payouts, and agencies that simplify fast and compliant global payments with low, flat-rate fees. Reach out to the Payment Labs team today to solve cross-border payments in your business the right way.