What is an FBO Account?

In the ever-evolving landscape of financial technology, businesses, especially small and medium-sized enterprises (SMBs), are seeking efficient ways to make payments.

In the ever-evolving landscape of financial technology (fintech), businesses, especially small and medium-sized enterprises (SMBs), are constantly seeking efficient and compliant ways to make domestic and international payments. One critical aspect of this process often involves the use of FBO (For Benefit Of) accounts. In this comprehensive blog post, we’ll delve into what FBO accounts are, how they are relevant to SMBs utilizing fintech platforms for payments, and why payment processors may require you to deposit funds in an FBO account before making payments.

Understanding FBO Accounts

What is an FBO Account?

An FBO account, short for “For Benefit Of” account, is a specialized type of bank account that is established for the benefit of a specific individual, entity, or organization. Unlike typical bank accounts, where the account holder has full ownership and control, an FBO account is held and managed by a custodian or trustee on behalf of the beneficiary.

Key Elements of an FBO Account

To understand how FBO accounts work, let’s break down their key elements:

Beneficiary: The beneficiary is the party for whose benefit the FBO account is created. This can be an individual, an organization, a trust, or any entity legally entitled to receive the funds.

Custodian or Trustee: The custodian or trustee is the entity responsible for managing the FBO account. They have legal ownership of the account and oversee its operations, including deposits, withdrawals, and investments.

Ownership: Importantly, the FBO account is owned by the custodian or trustee, not the beneficiary. This legal distinction ensures that the funds in the account are held separately from the custodian’s own assets.

Use: Funds in an FBO account are typically earmarked for a specific purpose or benefit, as specified in the account agreement. This ensures that the funds are used in alignment with the beneficiary’s needs or objectives.

Control: The custodian or trustee is obligated by law to act in the best interests of the beneficiary. They make financial decisions and execute transactions on behalf of the beneficiary, safeguarding the assets in the account.

Use Cases of FBO Accounts

FBO accounts are versatile and can be employed in various financial and legal scenarios, including:

Minors’ Accounts: Under the Uniform Transfers to Minors Act (UTMA) or Uniform Gifts to Minors Act (UGMA), FBO accounts are used for minors, with the custodian managing the assets until the child reaches a certain age.

Trusts: FBO accounts are common components of trusts, allowing assets to be held and managed for the benefit of trust beneficiaries.

Charitable Giving: Donors may establish FBO accounts to hold and manage funds earmarked for charitable organizations or causes.

Estate Planning: FBO accounts can be integrated into estate planning strategies, ensuring that assets are managed for specific beneficiaries after the account owner’s passing.

Now that we’ve established the fundamentals of FBO accounts, let’s explore their relevance to SMBs leveraging fintech platforms for payments.

The Role of FBO Accounts in SMB Fintech Payments

Fintech Revolutionizes SMB Payments

The advent of fintech has revolutionized the way SMBs handle payments, offering innovative solutions that are faster, more cost-effective, and often more compliant than traditional banking methods. SMBs can now access a wide array of financial services, including domestic and international payments, through fintech platforms.

Compliance and Regulatory Requirements

Compliance with domestic and international financial regulations is a critical concern for SMBs engaging in cross-border transactions. Failure to adhere to these regulations can result in fines, legal repercussions, and reputational damage. Fintech platforms are designed to help SMBs navigate these complex regulatory landscapes and ensure compliance.

The Need for Secure Fund Handling

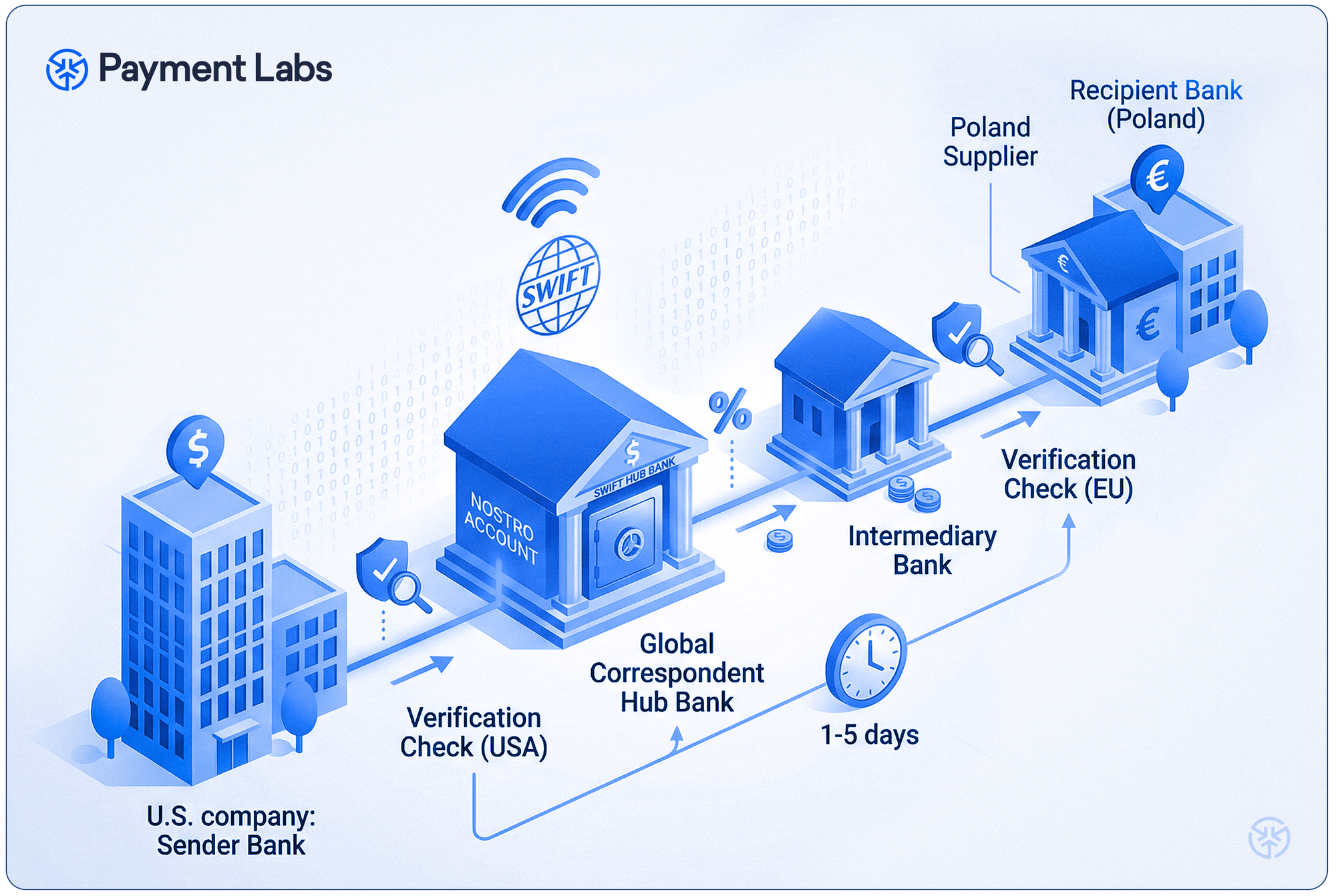

One of the key challenges in international payments is ensuring the secure handling of funds. This is where FBO accounts come into play. Fintech platforms often require SMBs to deposit funds into FBO accounts before making payments, and here’s why:

Why Payment Processors Require FBO Accounts

1. Risk Mitigation

When an SMB uses a fintech platform to make international payments, it involves multiple intermediaries and various regulatory jurisdictions. Payment processors require FBO accounts as a risk mitigation strategy. Here’s how it works:

Segregation of Funds: FBO accounts ensure the segregation of funds. By keeping the SMB’s funds separate from the payment processor’s operational accounts, any potential financial issues or disputes between the SMB and the payment processor won’t jeopardize the funds earmarked for payments.

Transparency: FBO accounts provide transparency and accountability. Both the SMB and the payment processor can easily track funds dedicated to specific transactions, enhancing transparency and trust.

2. Regulatory Compliance

Cross-border payments involve complex regulations related to anti-money laundering (AML) and know-your-customer (KYC) requirements. Fintech platforms and payment processors must comply with these regulations to avoid legal issues. FBO accounts play a crucial role in ensuring compliance by:

Source Verification: Funds deposited into FBO accounts are subject to rigorous source verification. Payment processors can trace the origin of funds, ensuring they are not linked to illicit activities.

Audit Trail: FBO accounts create an audit trail for regulatory authorities. This transparency simplifies compliance audits and investigations, reducing the risk of regulatory penalties.

3. Payment Execution

FBO accounts streamline the payment execution process. When an SMB initiates an international payment through a fintech platform, the payment processor can access the necessary funds in the FBO account to complete the transaction swiftly and efficiently. This minimizes delays and ensures that payments are processed without interruption.

FBO Account Best Practices for SMBs

As SMBs engage with fintech platforms and payment processors that require FBO accounts, it’s essential to follow best practices:

1. Partner with Reputable Providers

Select fintech platforms and payment processors with established track records for compliance and security. Research providers thoroughly, read reviews, and seek referrals to ensure your chosen partner is reputable.

2. Understand Fee Structures

FBO accounts may come with fees for account maintenance and transactions. SMBs should have a clear understanding of the fee structure and ensure it aligns with their budget and payment volume.

3. Maintain Clear Records

Maintain meticulous records of all transactions involving the FBO account. This includes deposit receipts, withdrawal records, and transaction history. Clear records are crucial for accounting, tax reporting, and compliance purposes.

4. Stay Informed About Regulations

Stay informed about domestic and international financial regulations, as they can change over time. Regularly review compliance requirements to ensure your business remains in full compliance.

Understanding why a payment processor may ask you to use FBO accounts to deposit funds can help you feel more at ease in the fast-paced world of SMB finance. FBO accounts are crucial tools for fintech platforms to execute secure and compliant payments both internationally and domestically. SMBs can benefit from these accounts by enhancing fund security, ensuring regulatory compliance, and streamlining payment execution.

As fintech continues to evolve, SMBs should leverage the expertise of fintech platforms and payment processors to navigate the complexities of cross-border payments effectively. With proper understanding and adherence to FBO account best practices, SMBs can confidently engage in international business transactions, knowing that their funds are secure and compliant with the relevant regulations.